Monetary policy is the process by which the monetary authority of a country controls the supply of money, often targeting a rate of interest for the purpose of promoting economic growth and stability. The official goals usually include relatively stable prices and low unemployment. Monetary theory provides insight into how to craft optimal monetary policy.

Monetary Policy

Monetary policy is referred to as either being expansionary or contractionary, where an expansionary policy increases the total supply of money in the economy more rapidly than usual, and contractionary policy expands the money supply more slowly than usual or even shrinks it. Expansionary policy is traditionally used to try to combat unemployment in a recession by lowering interest rates in the hope that easy credit will entice businesses into expanding. Contractionary policy is intended to slow inflation in hopes of avoiding the resulting distortions and deterioration of asset values.

Monetary policy differs from fiscal policy, which refers to taxation, government spending, and associated borrowing.

Monetary policy rests on the relationship between the rates of interest in an economy, that is, the price at which money can be borrowed, and the total supply of money. Monetary policy uses a variety of tools to control one or both of these, to influence outcomes like economic growth, inflation, exchange rates with other currencies and unemployment. Where currency is under a monopoly of issuance, or where there is a regulated system of issuing currency through banks which are tied to a central bank, the monetary authority has the ability to alter the money supply and thus influence the interest rate (to achieve policy goals). The beginning of monetary policy as such comes from the late 19th century, where it was used to maintain the gold standard.

A policy is referred to as contractionary if it reduces the size of the money supply or increases it only slowly, or if it raises the interest rate. An expansionary policy increases the size of the money supply more rapidly, or decreases the interest rate. Furthermore, monetary policies are described as follows: accommodative, if the interest rate set by the central monetary authority is intended to create economic growth; neutral, if it is intended neither to create growth nor combat inflation; or tight if intended to reduce inflation.

There are several monetary policy tools available to achieve these ends: increasing interest rates by fiat; reducing the monetary base; and increasing reserve requirements. All have the effect of contracting the money supply; and, if reversed, expand the money supply. Since the 1970s, monetary policy has generally been formed separately from fiscal policy. Even prior to the 1970s, the Bretton Woods system still ensured that most nations would form the two policies separately.

Within almost all modern nations, special institutions (such as the Federal Reserve System in the United States, the Bank of England, the European Central Bank, the People's Bank of China, and the Bank of Japan) exist which have the task of executing the monetary policy and often independently of the executive. In general, these institutions are called central banks and often have other responsibilities such as supervising the smooth operation of the financial system.

The primary tool of monetary policy is open market operations. This entails managing the quantity of money in circulation through the buying and selling of various financial instruments, such as treasury bills, company bonds, or foreign currencies. All of these purchases or sales result in more or less base currency entering or leaving market circulation.

Usually, the short term goal of open market operations is to achieve a specific short term interest rate target. In other instances, monetary policy might instead entail the targeting of a specific exchange rate relative to some foreign currency or else relative to gold. For example, in the case of the USA the Federal Reserve targets the federal funds rate, the rate at which member banks lend to one another overnight; however, the monetary policy of China is to target the exchange rate between the Chinese renminbi and a basket of foreign currencies.

The other primary means of conducting monetary policy include: (i) Discount window lending (lender of last resort); (ii) Fractional deposit lending (changes in the reserve requirement); (iii) Moral suasion (cajoling certain market players to achieve specified outcomes); (iv) "Open mouth operations" (talking monetary policy with the market).

Theory of Money Policy:

Monetary policy is the process by which the government, central bank, or monetary authority of a country controls (i) the supply of money, (ii) availability of money, and (iii) cost of money or rate of interest to attain a set of objectives oriented towards the growth and stability of the economy. Monetary theory provides insight into how to craft optimal monetary policy.

Monetary policy rests on the relationship between the rates of interest in an economy, that is the price at which money can be borrowed, and the total supply of money. Monetary policy uses a variety of tools to control one or both of these, to influence outcomes like economic growth, inflation, exchange rates with other currencies and unemployment. Where currency is under a monopoly of issuance, or where there is a regulated system of issuing currency through banks which are tied to a central bank, the monetary authority has the ability to alter the money supply and thus influence the interest rate (to achieve policy goals).

It is important for policymakers to make credible announcements. If private agents (consumers and firms) believe that policymakers are committed to lowering inflation, they will anticipate future prices to be lower than otherwise (how those expectations are formed is an entirely different matter; compare for instance rational expectations with adaptive expectations). If an employee expects prices to be high in the future, he or she will draw up a wage contract with a high wage to match these prices. Hence, the expectation of lower wages is reflected in wage-setting behavior between employees and employers (lower wages since prices are expected to be lower) and since wages are in fact lower there is no demand pull inflation because employees are receiving a smaller wage and there is no cost push inflation because employers are paying out less in wages.

To achieve this low level of inflation, policymakers must have credible announcements; that is, private agents must believe that these announcements will reflect actual future policy. If an announcement about low-level inflation targets is made but not believed by private agents, wage-setting will anticipate high-level inflation and so wages will be higher and inflation will rise. A high wage will increase a consumer's demand (demand pull inflation) and a firm's costs (cost push inflation), so inflation rises. Hence, if a policymaker's announcements regarding monetary policy are not credible, policy will not have the desired effect.

If policymakers believe that private agents anticipate low inflation, they have an incentive to adopt an expansionist monetary policy (where the marginal benefit of increasing economic output outweighs the marginal cost of inflation); however, assuming private agents have rational expectations, they know that policymakers have this incentive. Hence, private agents know that if they anticipate low inflation, an expansionist policy will be adopted that causes a rise in inflation. Consequently, (unless policymakers can make their announcement of low inflation credible), private agents expect high inflation. This anticipation is fulfilled through adaptive expectation (wage-setting behavior);so, there is higher inflation (without the benefit of increased output). Hence, unless credible announcements can be made, expansionary monetary policy will fail.

Announcements can be made credible in various ways. One is to establish an independent central bank with low inflation targets (but no output targets). Hence, private agents know that inflation will be low because it is set by an independent body. Central banks can be given incentives to meet targets (for example, larger budgets, a wage bonus for the head of the bank) to increase their reputation and signal a strong commitment to a policy goal. Reputation is an important element in monetary policy implementation. But the idea of reputation should not be confused with commitment.

While a central bank might have a favorable reputation due to good performance in conducting monetary policy, the same central bank might not have chosen any particular form of commitment (such as targeting a certain range for inflation). Reputation plays a crucial role in determining how much markets would believe the announcement of a particular commitment to a policy goal but both concepts should not be assimilated. Also, note that under rational expectations, it is not necessary for the policymaker to have established its reputation through past policy actions; as an example, the reputation of the head of the central bank might be derived entirely from his or her ideology, professional background, public statements, etc.

In fact it has been argued that to prevent some pathologies related to the time inconsistency of monetary policy implementation (in particular excessive inflation), the head of a central bank should have a larger distaste for inflation than the rest of the economy on average. Hence the reputation of a particular central bank is not necessary tied to past performance, but rather to particular institutional arrangements that the markets can use to form inflation expectations.

Despite the frequent discussion of credibility as it relates to monetary policy, the exact meaning of credibility is rarely defined. Such lack of clarity can serve to lead policy away from what is believed to be the most beneficial. For example, capability to serve the public interest is one definition of credibility often associated with central banks. The reliability with which a central bank keeps its promises is also a common definition. While everyone most likely agrees a central bank should not lie to the public, wide disagreement exists on how a central bank can best serve the public interest. Therefore, lack of definition can lead people to believe they are supporting one particular policy of credibility when they are really supporting another.

History of monetary policy:

Monetary policy is associated with interest rates and availabilility of credit. Instruments of monetary policy have included short-term interest rates and bank reserves through the monetary base. For many centuries there were only two forms of monetary policy: (i) Decisions about coinage; (ii) Decisions to print paper money to create credit. Interest rates, while now thought of as part of monetary authority, were not generally coordinated with the other forms of monetary policy during this time. Monetary policy was seen as an executive decision, and was generally in the hands of the authority with seigniorage, or the power to coin. With the advent of larger trading networks came the ability to set the price between gold and silver, and the price of the local currency to foreign currencies. This official price could be enforced by law, even if it varied from the market price.

Paper money called "jiaozi" originated from promissory notes in 7th century China. Jiaozi did not replace metallic currency, and were used alongside the copper coins. The successive Yuan Dynasty was the first government to use paper currency as the predominant circulating medium. In the later course of the dynasty, facing massive shortages of specie to fund war and their rule in China, they began printing paper money without restrictions, resulting in hyperinflation.

With the creation of the Bank of England in 1694, which acquired the responsibility to print notes and back them with gold, the idea of monetary policy as independent of executive action began to be established. The goal of monetary policy was to maintain the value of the coinage, print notes which would trade at par to specie, and prevent coins from leaving circulation. The establishment of central banks by industrializing nations was associated then with the desire to maintain the nation's peg to the gold standard, and to trade in a narrow band with other gold-backed currencies. To accomplish this end, central banks as part of the gold standard began setting the interest rates that they charged, both their own borrowers, and other banks who required liquidity. The maintenance of a gold standard required almost monthly adjustments of interest rates.

During the 1870-1920 period, the industrialized nations set up central banking systems, with one of the last being the Federal Reserve in 1913. By this point the role of the central bank as the "lender of last resort" was understood. It was also increasingly understood that interest rates had an effect on the entire economy, in no small part because of the marginal revolution in economics, which demonstrated how people would change a decision based on a change in the economic trade-offs.

Monetarist macroeconomists have sometimes advocated simply increasing the monetary supply at a low, constant rate, as the best way of maintaining low inflation and stable output growth. However, when U.S. Federal Reserve Chairman Paul Volcker tried this policy, starting in October 1979, it was found to be impractical, because of the highly unstable relationship between monetary aggregates and other macroeconomic variables. Even Milton Friedman acknowledged that money supply targeting was less successful than he had hoped, in an interview with the Financial Times on June 7, 2003. Therefore, monetary decisions today take into account a wider range of factors, such as:

* short term interest rates;

* long term interest rates;

* velocity of money through the economy;

* exchange rates;

* credit quality;

* bonds and equities (corporate ownership and debt);

* government versus private sector spending/savings;

* international capital flows of money on large scales;

* financial derivatives such as options, swaps, futures contracts, etc.

A small but vocal group of people, primarily libertarians and Constitutionalists, advocate for a return to the gold standard (the elimination of the dollar's fiat currency status and even of the Federal Reserve Bank). Their argument is basically that monetary policy is fraught with risk and these risks will result in drastic harm to the populace should monetary policy fail. Others[who?] see another problem with our current monetary policy. The problem for them is not that our money has nothing physical to define its value, but that fractional reserve lending of that money as a debt to the recipient, rather than a credit, causes all but a small proportion of society (including all governments) to be perpetually in debt.

In fact, many economists[who?] disagree with returning to a gold standard. They argue that doing so would drastically limit the money supply, and throw away 100 years of advancement in monetary policy. The sometimes complex financial transactions that make big business (especially international business) easier and safer would be much more difficult if not impossible. Moreover, shifting risk to different people/companies that specialize in monitoring and using risk can turn any financial risk into a known dollar amount and therefore make business predictable and more profitable for everyone involved. Some have claimed that these arguments lost credibility in the global financial crisis of 2008-2009.

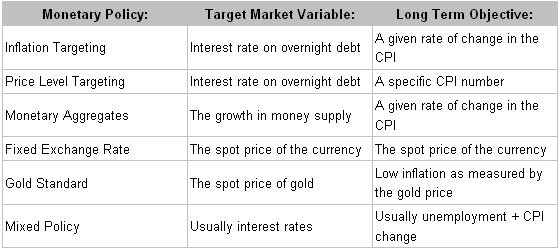

Types of monetary policy:

In practice, to implement any type of monetary policy the main tool used is modifying the amount of base money in circulation. The monetary authority does this by buying or selling financial assets (usually government obligations). These open market operations change either the amount of money or its liquidity (if less liquid forms of money are bought or sold). The multiplier effect of fractional reserve banking amplifies the effects of these actions.

Constant market transactions by the monetary authority modify the supply of currency and this impacts other market variables such as short term interest rates and the exchange rate.

The distinction between the various types of monetary policy lies primarily with the set of instruments and target variables that are used by the monetary authority to achieve their goals.

In practice, to implement any type of monetary policy the main tool used is modifying the amount of base money in circulation. The monetary authority does this by buying or selling financial assets (usually government obligations). These open market operations change either the amount of money or its liquidity (if less liquid forms of money are bought or sold). The multiplier effect of fractional reserve banking amplifies the effects of these actions.

Constant market transactions by the monetary authority modify the supply of currency and this impacts other market variables such as short term interest rates and the exchange rate.

The distinction between the various types of monetary policy lies primarily with the set of instruments and target variables that are used by the monetary authority to achieve their goals.

The different types of policy are also called monetary regimes, in parallel to exchange rate regimes. A fixed exchange rate is also an exchange rate regime; The Gold standard results in a relatively fixed regime towards the currency of other countries on the gold standard and a floating regime towards those that are not. Targeting inflation, the price level or other monetary aggregates implies floating exchange rate unless the management of the relevant foreign currencies is tracking exactly the same variables (such as a harmonized consumer price index).